Short term is a period of time during which some factors of production are constant and others are variable.

Fixed factors include fixed assets and the number of firms operating in the industry. During this period, the company has the opportunity to vary only the degree of utilization of production capacity.

Long term is a period of time during which all factors are variable. In the long term, a company has the opportunity to change the overall size of buildings, structures, the amount of equipment, and the industry - the number of firms operating in it.

Fixed costs (FC) - these are costs, the value of which in the short term does not change with an increase or decrease in production volume.

Fixed costs include costs associated with the use of buildings and structures, machinery and production equipment, rent, major repairs, as well as administrative expenses.

Because As production volume increases, total revenue increases, then average fixed costs (AFC) represent a decreasing value.

Variable costs (VC) - these are costs, the value of which changes depending on the increase or decrease in production volume.

Variable costs include the cost of raw materials, electricity, auxiliary materials, and labor.

Average variable costs (AVC) are:

Total costs (TC) – a set of fixed and variable costs of the company.

Total costs are a function of output produced:

TC = f (Q), TC = FC + VC.

Graphically, total costs are obtained by summing the curves of fixed and variable costs (Fig. 6.1).

Average total cost is: ATC = TC/Q or AFC +AVC = (FC + VC)/Q.

Graphically, ATC can be obtained by summing the AFC and AVC curves.

Marginal Cost (MC) is the increase in total costs caused by an infinitesimal increase in production. Marginal cost usually refers to the cost associated with producing an additional unit of output.

20. Long-run production costs

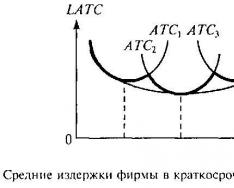

The main feature of costs in the long run is the fact that they are all variable in nature - the firm can increase or reduce capacity, and it also has enough time to decide to leave a given market or enter it by moving from another industry. Therefore, in the long run, average fixed and average variable costs are not distinguished, but average costs per unit of production (LATC) are analyzed, which in essence are also average variable costs.

To illustrate the situation with costs in the long run, consider a conditional example. Some enterprise expanded over a fairly long period of time, increasing its production volumes. The process of expanding the scale of activity will be conditionally divided into three short-term stages within the analyzed long-term period, each of which corresponds to different enterprise sizes and volumes of output. For each of the three short-term periods, short-term average cost curves can be constructed for different enterprise sizes - ATC 1, ATC 2 and ATC 3. The general average cost curve for any volume of production will be a line consisting of the outer parts of all three parabolas - graphs of short-term average costs.

In the example considered, we used a situation with a 3-stage expansion of the enterprise. A similar situation can be assumed not for 3, but for 10, 50, 100, etc. short-term periods within a given long-term period. Moreover, for each of them you can draw the corresponding ATS graphs. That is, we will actually get a lot of parabolas, a large set of which will lead to the alignment of the outer line of the average cost graph, and it will turn into a smooth curve - LATC. Thus, long-run average cost (LATC) curve represents a curve that envelops an infinite number of short-term average production cost curves that touch it at their minimum points. The long-run average cost curve shows the lowest cost per unit of production at which any level of output can be achieved, provided that the firm has time to change all factors of production.

In the long run there are also marginal costs. Long Run Marginal Cost (LMC) show the change in the total amount of costs of the enterprise in connection with a change in the volume of output of finished products by one unit in the case when the company is free to change all types of costs.

The long-run average and marginal cost curves relate to each other in the same way as the short-run cost curves: if LMC lies below LATC, then LATC falls, and if LMC lies above laTC, then laTC rises. The rising portion of the LMC curve intersects the LATC curve at the minimum point.

There are three segments on the LATC curve. In the first of them, long-term average costs are reduced, in the third, on the contrary, they increase. It is also possible that there will be an intermediate segment on the LATC chart with approximately the same level of costs per unit of output at different values of output volume - Q x. The arcuate nature of the long-term average cost curve (the presence of decreasing and increasing sections) can be explained using patterns called positive and negative effects of increased scale of production or simply scale effects.

The positive effect of scale of production (the effect of mass production, economies of scale, increasing returns to scale of production) is associated with a decrease in costs per unit of production as production volumes increase. Increasing returns to scale of production (positive economies of scale) occurs in a situation where output (Q x) grows faster than costs rise, and therefore the enterprise's LATC falls. The existence of a positive effect of scale of production explains the descending nature of the LATS graph in the first segment. This is explained by the expansion of the scale of activity, which entails:

1. Increased labor specialization. Labor specialization presupposes that diverse production responsibilities are divided among different workers. Instead of carrying out several different production operations at the same time, which would be the case with a small-scale enterprise, in conditions of mass production each worker can limit himself to one single function. This results in an increase in labor productivity and, consequently, a reduction in costs per unit of production.

2. Increased specialization of managerial work. As the size of an enterprise grows, the opportunity to take advantage of specialization in management increases, when each manager can focus on one task and perform it more efficiently. This ultimately increases the efficiency of the enterprise and entails a reduction in costs per unit of production.

3. Efficient use of capital (means of production). The most efficient equipment from a technological point of view is sold in the form of large, expensive kits and requires large production volumes. The use of this equipment by large manufacturers allows them to reduce costs per unit of production. Such equipment is not available to small firms due to low production volumes.

4. Savings from using secondary resources. A large enterprise has more opportunities to produce by-products than a small company. A large firm thus makes more efficient use of the resources involved in production. Hence the lower costs per unit of production.

The positive effect of scale of production in the long run is not unlimited. Over time, the expansion of an enterprise can lead to negative economic consequences, causing a negative effect of scale of production, when the expansion of the volume of a company's activities is associated with an increase in production costs per unit of output. Diseconomies of scale occurs when production costs rise faster than production volume and, therefore, LATC rises as output increases. Over time, an expanding company may encounter negative economic facts caused by the complication of the enterprise management structure - the management floors separating the administrative apparatus and the production process itself are multiplying, top management turns out to be significantly removed from the production process at the enterprise. Problems arise related to the exchange and transmission of information, poor coordination of decisions, and bureaucratic red tape. The effectiveness of interaction between individual divisions of the company decreases, management flexibility is lost, control over the implementation of decisions made by the company's management becomes more complicated and difficult. As a result, the operating efficiency of the enterprise decreases, and average production costs increase. Therefore, when planning its production activities, a company needs to determine the limits of expanding the scale of production.

In practice, cases are possible when the LATC curve is parallel to the x-axis at a certain interval - on the graph of long-term average costs there is an intermediate segment with approximately the same level of costs per unit of output for different values of Q x. Here we are dealing with constant returns to scale of production. Constant returns to scale occurs when costs and output grow at the same rate and, therefore, LATC remains constant at all output levels.

The appearance of the long-term cost curve allows us to draw some conclusions about the optimal enterprise size for different sectors of the economy. Minimum effective scale (size) of an enterprise- the level of output from which the effect of savings due to an increase in the scale of production ceases. In other words, we are talking about such values of Q x at which the company achieves the lowest costs per unit of production. The level of long-term average costs determined by the effect of economies of scale affects the formation of the effective size of the enterprise, which, in turn, affects the structure of the industry. To understand, consider the following three cases.

1. The long-term average cost curve has a long intermediate segment, for which the LATC value corresponds to a certain constant (Figure a). This situation is characterized by a situation where enterprises with production volumes from Q A to Q B have the same cost. This is typical for industries that include enterprises of different sizes, and the level of average production costs for them will be the same. Examples of such industries: wood processing, timber industry, food production, clothing, furniture, textiles, petrochemical products.

2. The LATC curve has a fairly long first (descending) segment, in which there is a positive effect of production scale (Figure b). The minimum cost is achieved with large production volumes (Q c). If the technological features of the production of certain goods give rise to a long-term average cost curve of the described form, then large enterprises will be present in the market for these goods. This is typical, first of all, for capital-intensive industries - metallurgy, mechanical engineering, automotive industry, etc. Significant economies of scale are also observed in the production of standardized products - beer, confectionery, etc.

3. The falling segment of the long-term average costs graph is very insignificant; the negative effect of scale of production quickly begins to work (Figure c). In this situation, the optimal production volume (Q D) is achieved with a small volume of output. If there is a large-capacity market, we can assume the possibility of the existence of many small enterprises producing this type of product. This situation is typical for many sectors of the light and food industries. Here we are talking about non-capital-intensive industries - many types of retail trade, farms, etc.

|

§ 4. MINIMIZATION OF COSTS: CHOICE OF PRODUCTION FACTORS |

|

At the long-term stage, if production capacity is increased, each firm faces the problem of a new ratio of production factors. The essence of this problem is to ensure a predetermined volume of production at minimal cost. To study this procedure, let us assume that there are only two factors of production: capital K and labor L. It is not difficult to understand that the price of labor determined in competitive markets is equal to the wage rate w. The price of capital is equal to the rental price for equipment r. To simplify the study, we assume that all equipment (capital) is not purchased by the company, but is rented, for example, through a leasing system, and that the prices for capital and labor remain constant within a given period. Production costs can be presented in the form of so-called “isocosts”. They are understood as all possible combinations of labor and capital that have the same total cost, or, what is the same, combinations of factors of production with equal total costs.

Rice. 7.5. The quantity of output as a function of minimum production costs. The firm cannot choose the isocost C0, since there is no combination of factors that would ensure the output of products Q at their cost equal to C0. A given volume of production can be achieved at costs equal to C2, when labor and capital costs are respectively equal to L2 and K2 or L3 and K3. But in this case, the costs will not be minimal, which does not meet the goal. The solution at point N will be significantly more effective, since in this case the set of production factors will ensure the minimization of production costs. The above is true provided that the prices of factors of production are constant. In practice this does not happen. Let's assume that the price of capital increases. Then the slope of the isocost, equal to w/r, will decrease, and the C1 curve will become flatter. Minimization of costs in this case will take place at point M with values L4 and K4. |

As the price of capital increases, the firm substitutes labor for capital. The marginal rate of technological substitution is the amount by which capital costs can be reduced by using an additional unit of labor while maintaining a constant volume of production. The rate of technological substitution is designated MPTS. In economic theory it has been proven that it is equal to the slope of the isoquant with the opposite sign. Then MPTS = ?K / ?L = MPL / MPk. Through simple transformations we obtain: MPL / w = MPK / r, where MP is the marginal product of capital or labor. From the last equation it follows that at minimum costs, each additional ruble spent on production factors produces an equal amount of output. It follows that under the above conditions, a firm can choose between factors of production and buy a cheaper factor, which will correspond to a certain structure of factors of production

Let's start by considering the fundamental problem that all firms face: how to choose the combination of factors to achieve a certain level of output at minimum cost. To simplify, let's take two variable factors: labor (measured in hours of work) and capital (measured in hours of use of machinery and equipment). We assume that both labor and capital can be hired or rented in competitive markets. The price of labor is equal to the wage rate w, and the price of capital is equal to the rent for equipment r. We assume that capital is "rented" rather than purchased, and can therefore put all business decisions on a comparative basis. Since labor and capital are attracted competitively, we assume the price of these factors to be constant. We can then focus on the optimal combination of factors of production without worrying that large purchases will cause a jump in the prices of the factors of production used.

22 Determining Price and Output in a Competitive Industry and in a Pure Monopoly A pure monopoly promotes inequality in the distribution of income in society as a result of monopoly market power and charging higher prices at the same costs than in pure competition, which allows for monopoly profits. In conditions of market power, it is possible for a monopolist to use price discrimination, when different prices are set for different buyers. Many of the purely monopolistic firms are natural monopolies, which are subject to mandatory government regulation in accordance with antitrust laws. To study the case of a regulated monopoly, we use graphs of demand, marginal revenue and costs of a natural monopoly, which operates in an industry where positive economies of scale occur at all output volumes. The higher the firm's output, the lower its average ATC costs. Due to this change in average costs, the marginal costs of MC for all volumes of production will be lower than average costs. This is explained by the fact that, as we have established, the marginal cost graph intersects the average cost graph at the minimum point of the ATC, which is absent in this case. We show the determination of the optimal volume of production by a monopolist and possible methods of regulating it in Fig. Price, marginal revenue (marginal income) and costs of a regulated monopoly As can be seen from the graphs, if this natural monopoly were unregulated, then the monopolist, in accordance with the rule MR = MC and the demand curve for its products, chose the quantity of products Qm and the price Pm, which allowed to get maximum gross profit. However, the price Pm would exceed the socially optimal price. The socially optimal price is the price that ensures the most efficient allocation of resources in society. As we established earlier in topic 4, it must correspond to marginal cost (P = MC). In Fig. this is the price Po at the intersection point of the demand schedule D and the marginal cost curve MC (point O). The production volume at this price is Qо. However, if government agencies fixed the price at the level of the socially optimal price Po, this would lead the monopolist to losses, since the price Po does not cover the average gross costs of the vehicle. To solve this problem, the following main options for regulating a monopolist are possible: Allocation of state subsidies from the budget of the monopoly industry to cover the gross loss in the case of establishing a fixed price at the socially optimal level. Granting the monopoly industry the right to conduct price discrimination in order to obtain additional income from more solvent consumers to cover the monopolist's losses. Setting the regulated price at a level that ensures normal profits. In this case, the price is equal to the average gross cost. In the figure, this is the price Pn at the intersection point of the demand schedule D and the average gross cost curve of the ATC. The output at the regulated price Pn is equal to Qn. The price Pn allows the monopolist to recover all economic costs, including making a normal profit.

23. This principle is based on two main points. First, the firm must decide whether it will produce the product. It should be produced if the company can make either a profit or a loss that is less than fixed costs. Secondly, you need to decide how much of the product should be produced. This production volume must either maximize profits or minimize losses. This technique uses formulas (1.1) and (1.2). Next, you should produce such a volume of production Qj that maximizes profit R, i.e.: R(Q) ^max. The analytical determination of the optimal production volume is as follows: R, (Qj) = PMj Qj - (TFCj + UVCj QY). Let us equate the partial derivative with respect to Qj to zero: dR, (Q,) = 0 dQ, " (1.3) РМг - UVCj Y Qj-1 = 0. where Y is the coefficient of change in variable costs. The value of gross variable costs changes depending on the change in volume production. The increase in the amount of variable costs associated with an increase in production volume by one unit is not constant. It is assumed that variable costs increase at an increasing rate. This is due to the fact that constant resources are fixed, and in the process of production growth, variable resources increase. marginal productivity falls and, therefore, variable costs increase at an increasing pace. “To calculate variable costs, it is proposed to apply a formula, and based on the results of statistical analysis, it has been established that the coefficient of change in variable costs (Y) is limited to the interval 1.< Y < 1,5" . При Y = 1 переменные издержки растут линейно: TVCг = UVCjQY, г = ЇЯ (1.4) где TVCг - переменные издержки на производство продукции i-го вида. Из (1.3) получаем оптимальный объем производства товара i-го вида: 1 f РМг } Y-1 QOPt = v UVCjY , После этого сравнивается объем Qг с максимально возможным объемом производства Qjmax: Если Qг < Qjmax, то базовая цена Рг = РМг. Если Qг >Qjmax, then, if there is a production volume Qg at which: Rj(Qj) > 0, then Рg = PMh Rj(Qj)< 0, то возможны два варианта: отказ от производства i-го товара; установление Рг >RMg. The difference between this method and approach 1.2 is that here the optimal sales volume is determined at a given price. It is then also compared to the maximum "market" sales volume. The disadvantage of this method is the same as that of 1.2 - it does not take into account the entire possible composition of the enterprise’s products in conjunction with its technological capabilities.

The division of costs into fixed and variable is the basis of a method that is widespread in economics. It was first proposed in 1930 by engineer Walter Rautenstrauch as a planning method known as the critical production schedule or break-even schedule (Fig. 19).

The break-even chart in its various modifications is widely used in modern economics. The undoubted advantage of this method is that with its help you can quickly obtain a fairly accurate forecast of the main performance indicators of an enterprise when market conditions change.

When constructing a break-even schedule, it is assumed that there are no changes in prices for raw materials and products during the period for which planning is carried out; fixed costs are considered constant over a limited range of sales volumes; variable costs per unit of output do not change as sales volume changes; sales are carried out quite evenly.

When plotting a graph, the horizontal axis shows the volume of production in units of products or as a percentage of production capacity utilization, and the vertical axis shows production costs and income. Costs are deferred and divided into fixed (POI) and variable (PI).

In addition to the lines of fixed and variable costs, the graph displays gross costs (VI) and revenue from sales of products (VR).

The point of intersection of the revenue and gross cost lines represents the break-even point (K). This point is interesting because with the corresponding volume of production and sales (V kr), the enterprise has neither profit nor loss. The production volume corresponding to the break-even point is called critical. When the production volume is less than critical, the enterprise cannot cover its costs with its revenue and, therefore, the result of its activities is losses. If the volume of production and sales exceeds the critical level, the enterprise makes a profit. The break-even point can be determined and.

analytical method

Revenue from product sales is determined by the expression Where POI – fixed costs; PI – variable costs; P

- profit.

If we take into account that at the break-even point profit is zero, then the point of critical production volume can be found using the formula

Revenue from product sales is determined by the expression Sales revenue is the product of sales volume and product price. The total amount of variable costs can be calculated as the product of variable costs per unit of production and the volume of production corresponding to sales volume. Since at the break-even point the volume of production (sales) is equal to the critical volume, the previous formula takes the following form: C – unit price; SPI – variable costs per unit of production; In kr

Using break-even analysis, you can not only calculate the critical production volume, but also the volume at which the planned (target) profit can be obtained. This method allows you to choose the best option when comparing several technologies, etc.

The benefits of dividing costs into fixed and variable parts are used by many modern enterprises. Along with this, cost accounting at full cost and their corresponding grouping are widely used.

Test control

1. If fixed costs increaseClassification of enterprise costs implies their division into two types: fixed and variable.

change in proportion to changes in production volumes. In practice, costs of one type may be variable for one enterprise, but constant for another.

Variable production costs

The growth or reduction of this variable cost depends on the dynamics of production volumes. Another name - proportional costs - is due to the fact that they increase and decrease in proportion to the increase or decrease in the volume of production activity.

- This type of costs includes:

- piecework wage costs;

- expenses for the purchase of raw materials;

- electricity costs;

transport, trade commissions and other expenses.

Fixed production costs

- The growth or reduction of this type of costs is practically not affected by production dynamics, but only up to a certain point. Fixed costs, which can also be called fixed or disproportionate, include:

- rent;

- payment of utilities;

- Administrative expenses;

- interest on loans;

- deductions for depreciation;

salaries of managers at different levels.

Variable costs may not increase as quickly as production and sales volumes. For example, when purchasing raw materials in larger volumes than usual, it is possible to receive large discounts.

An increase in fixed costs with an increase in sales volumes occurs at almost the same speed as a decrease with a decrease. With variable costs, the situation is different: with an increase in sales volumes, they increase faster than they decrease in the event of a decline in production. This is due to the fact that some of the expenses do not disappear immediately: employees still have to pay salaries for some time, and the released equipment needs to be maintained and stored. This phenomenon is called the remanent effect. Its essence is that the absolute value of variable costs decreases, but their specific size per unit of output decreases more slowly than the decline in production.

Cost price- the initial cost of the costs incurred by the enterprise for the production of a unit of product.

Price- the monetary equivalent of all types of costs including some types of variable costs.

Price- the market equivalent of the generally accepted cost of the product offered.

Production costs- these are expenses, monetary expenditures that must be made to create. For (the company) they act as payment for purchased goods.

Private and public costs

Costs can be viewed from different perspectives. If they are examined from the point of view of an individual firm (individual producer), we are talking about private costs. If costs are analyzed from the point of view of society as a whole, then, as a consequence, there arises the need to take into account social costs.

Let us clarify the concept of external effects. In market conditions, a special purchase and sale relationship arises between the seller and the buyer. At the same time, relationships arise that are not mediated by the commodity form, but have a direct impact on people’s well-being (positive and negative external effects). An example of positive external effects is expenses for R&D or training of specialists; an example of a negative external effect is compensation for damage from environmental pollution.

Social and private costs coincide only if there are no external effects, or if their total effect is equal to zero.

Social costs = Private costs + Externalities

Fixed Variables and Total Costs

Fixed costs- this is a type of cost that an enterprise incurs within one. Determined by the enterprise independently. All these costs will be typical for all product production cycles.

Variable costs- these are types of costs that are transferred to the finished product in full.

General costs- those costs incurred by the enterprise during one stage of production.

General = Constants + Variables

Opportunity Cost

Accounting and economic costs

Accounting costs- this is the cost of the resources used by the company in the actual prices of their acquisition.

Accounting costs = Explicit costs

Economic costs- this is the cost of other benefits (goods and services) that could be obtained with the most profitable possible alternative use of these resources.

Opportunity (economic) costs = Explicit costs + Implicit costs

These two types of costs (accounting and economic) may or may not coincide with each other.

If resources are purchased in a free competitive market, then the actual equilibrium market price paid for their acquisition is the price of the best alternative (if this were not the case, the resource would go to another buyer).

If resource prices are not equal to equilibrium due to market imperfections or government intervention, then actual prices may not reflect the cost of the best rejected alternative and may be higher or lower than opportunity costs.

Explicit and implicit costs

From the division of costs into alternative and accounting costs follows the classification of costs into explicit and implicit.

Explicit costs are determined by the amount of expenses for paying for external resources, i.e. resources not owned by the firm. For example, raw materials, materials, fuel, labor, etc. Implicit costs are determined by the cost of internal resources, i.e. resources owned by the firm.

An example of an implicit cost for an entrepreneur would be the salary that he could receive as an employee. For the owner of capital property (machinery, equipment, buildings, etc.), previously incurred expenses for its acquisition cannot be attributed to the explicit costs of the present period. However, the owner incurs implicit costs, since he could sell this property and put the proceeds in the bank at interest, or rent it out to a third party and receive income.

Implicit costs, which are part of economic costs, should always be taken into account when making current decisions.

Explicit costs- These are opportunity costs that take the form of cash payments to suppliers of factors of production and intermediate goods.

Explicit costs include:

- workers' wages

- cash costs for the purchase and rental of machines, equipment, buildings, structures

- payment of transportation costs

- communal payments

- payment to suppliers of material resources

- payment for services of banks, insurance companies

Implicit costs- these are the opportunity costs of using resources owned by the company itself, i.e. unpaid expenses.

Implicit costs can be represented as:

- cash payments that a company could receive if it uses its assets more profitably

- for the owner of capital, implicit costs are the profit that he could have received by investing his capital not in this, but in some other business (enterprise)

Returnable and sunk costs

Sunk costs are considered in a broad and narrow sense.

In a broad sense, sunk costs include those expenses that a company cannot return even if it ceases its activities (for example, costs of registering a company and obtaining a license, preparing an advertising sign or company name on the wall of a building, making seals, etc. .). Sunk costs are like a company's payment for entering or leaving the market.

In the narrow sense of the word sunk costs are the costs of those types of resources that have no alternative use. For example, the costs of specialized equipment manufactured to order from the company. Since the equipment has no alternative use, its opportunity cost is zero.

Sunk costs are not included in opportunity costs and do not influence the firm's current decisions.

Fixed costs

In the short run, some resources remain unchanged, while others change to increase or decrease total output.

In accordance with this, short-term economic costs are divided into fixed and variable costs. In the long run, this division becomes meaningless, since all costs can change (that is, they are variable).

Fixed costs- These are costs that do not depend in the short term on how much the firm produces. They represent the costs of its constant factors of production.

Fixed costs include:

- payment of interest on bank loans;

- depreciation deductions;

- payment of interest on bonds;

- salary of management personnel;

- rent;

- insurance payments;

Variable costs

Variable costs- These are costs that depend on the volume of production of the company. They represent the costs of the firm's variable factors of production.

Variable costs include:

- fare

- electricity costs

- raw materials costs

From the graph we see that the wavy line depicting variable costs rises with increasing production volume.

This means that as production increases, variable costs increase:

General (gross) costs

General (gross) costs- these are all the costs at a given time necessary for a particular product.

Total costs (total cost) represent the firm's total expenses for paying for all factors of production.

Total costs depend on the volume of output and are determined by:

- quantity;

- market price of the resources used.

The relationship between the volume of output and the volume of total costs can be represented as a cost function:

which is the inverse function of the production function.

Classification of total costs

Total costs are divided into:

total fixed costs(!!TFC??, total fixed cost) - the company’s total costs for all fixed factors of production.

total variable costs(, total variabl cost) - the company’s total expenses on variable factors of production.

Thus,

At zero output (when the firm is just starting production or has already ceased operations), TVC = 0, and, therefore, total costs coincide with total fixed costs.

Graphically, the relationship between total, fixed and variable costs can be depicted, similar to how it is shown in the figure.

Graphical representation of costs

The U-shape of the short-term ATC, AVC and MC curves is an economic pattern and reflects law of diminishing returns, according to which the additional use of a variable resource with a constant amount of a constant resource leads, starting from a certain point in time, to a reduction in marginal returns, or marginal product.

As has already been proven above, marginal product and marginal costs are inversely related, and, therefore, this law of decreasing marginal product can be interpreted as the law of increasing marginal costs. In other words, this means that starting at some point in time, additional use of a variable resource leads to an increase in marginal and average variable costs, as shown in Fig. 2.3.

Rice. 2.3. Average and marginal costs of production

The marginal cost curve MC always intersects the lines of average (ATC) and average variable costs (AVC) at their minimum points, just as average product curve AP always intersects the marginal product curve MP at its maximum point. Let's prove it.

Average total costs ATC=TC/Q.

Marginal cost MS=dTC/dQ.

Let us take the derivative of average total costs with respect to Q and obtain

Thus:

- if MC > ATC, then (ATS)" > 0, and the average total cost curve of ATC increases;

- if MS< AТС, то (АТС)" <0 , и кривая АТС убывает;

- if MC = ATC, then (ATS)"=0, i.e. the function is at the extremum point, in this case at the minimum point.

In a similar way, you can prove the relationship between average variable costs (AVC) and marginal costs (MC) on the graph.

Costs and price: four models of firm development

Analysis of the profitability of individual enterprises in the short term allows us to distinguish four models of development of an individual company, depending on the ratio of the market price and its average costs:

1. If the firm’s average total costs are equal to the market price, i.e.

ATS=P,

then the firm earns “normal” profits, or zero economic profit.

Graphically this situation is depicted in Fig. 2.4.

Rice. 2.4. Normal profit

2. If favorable market conditions and high demand increase the market price so that

ATC< P

then the company receives positive economic profit, as shown in Figure 2.5.

Rice. 2.5. Positive economic profit

3. If the market price corresponds to the minimum average variable cost of the firm,

then the enterprise is located at the limit of expediency continuation of production. Graphically, a similar situation is shown in Figure 2.6.

Rice. 2.6. A firm at its limit

4. And finally, if market conditions are such that the price does not cover even the minimum level of average variable costs,

AVC>P,

It is advisable for the company to close its production, since in this case the losses will be less than if the production activity continues (more about this in the topic “Perfect competition”).

Calculators